Published June 2025

The 'Accelerating private investment in peatland restoration' Signpost Report discusses proposals for a more robust market around peatland including integration within the Emissions Trading Scheme (ETS) to accelerate private investment. You can also access a copy of 'Accelerating private investment in peatland restoration' in PDF format.

Summary

Peatland can capture and store carbon but degraded peatland releases that carbon: around 20 million tonnes of CO2 per year across the UK. Most peatland restoration is supported by public investment – increasingly blended with private sources. Landholders of peatland are not accountable for the emissions and it sits outside compulsory carbon markets. This paper proposes a more robust market around peatland including integration within the Emissions Trading Scheme (ETS) to accelerate private investment. As well as supporting Net Zero this would deliver a range of other outcomes including significant nature benefits.

Context

Between 1990 and 2024 the UK halved its greenhouse gas emissions, driven mostly by traditional polluting sectors such as energy (Defra 2024). Emissions from electricity generation fell by nearly a fifth from 2022 to 2023 alone. Yet as these sectors decarbonise the burden shifts to other sectors – with fewer opportunities to innovate around the problem (Climate Change Committee 2024). If government is to remain on track to reach Net Zero it must increasingly utilise nature-based solutions which are both cost effective and offer co-benefits such as improved air and water quality, flood prevention, and better health.

Peatland, which covers 12% of the UK, is both a challenge and a major opportunity. It can sequester carbon and over time has been a major sink. But when drained it releases that stored carbon to become a significant source of emissions. Reversing this by rewetting peatland is cost effective but still incurs an upfront cost, and often loss of income, which must be compensated.

Markets Today

Carbon markets, which shift the burden to polluters, exist in two broad forms: compliance-based and voluntary markets. Compliance-based pollution markets like the Emissions Trading Scheme (ETS) are mandatory but only cover some industries. ETS caps overall emissions and allows participants to trade allowances, shifting spending to the most cost effective abatement opportunities. It does not integrate sequestration.

Figure 1. Illustrative diagram of the process of compliance markets (adapted from EU Emissions Trading Scheme Explained, Investigate Europe website) Note: we ignore here markets which offset carbon emissions by paying another party to reduce their emissions. These are increasingly seen as “greenwashing” but see discussion of peatland markets below.

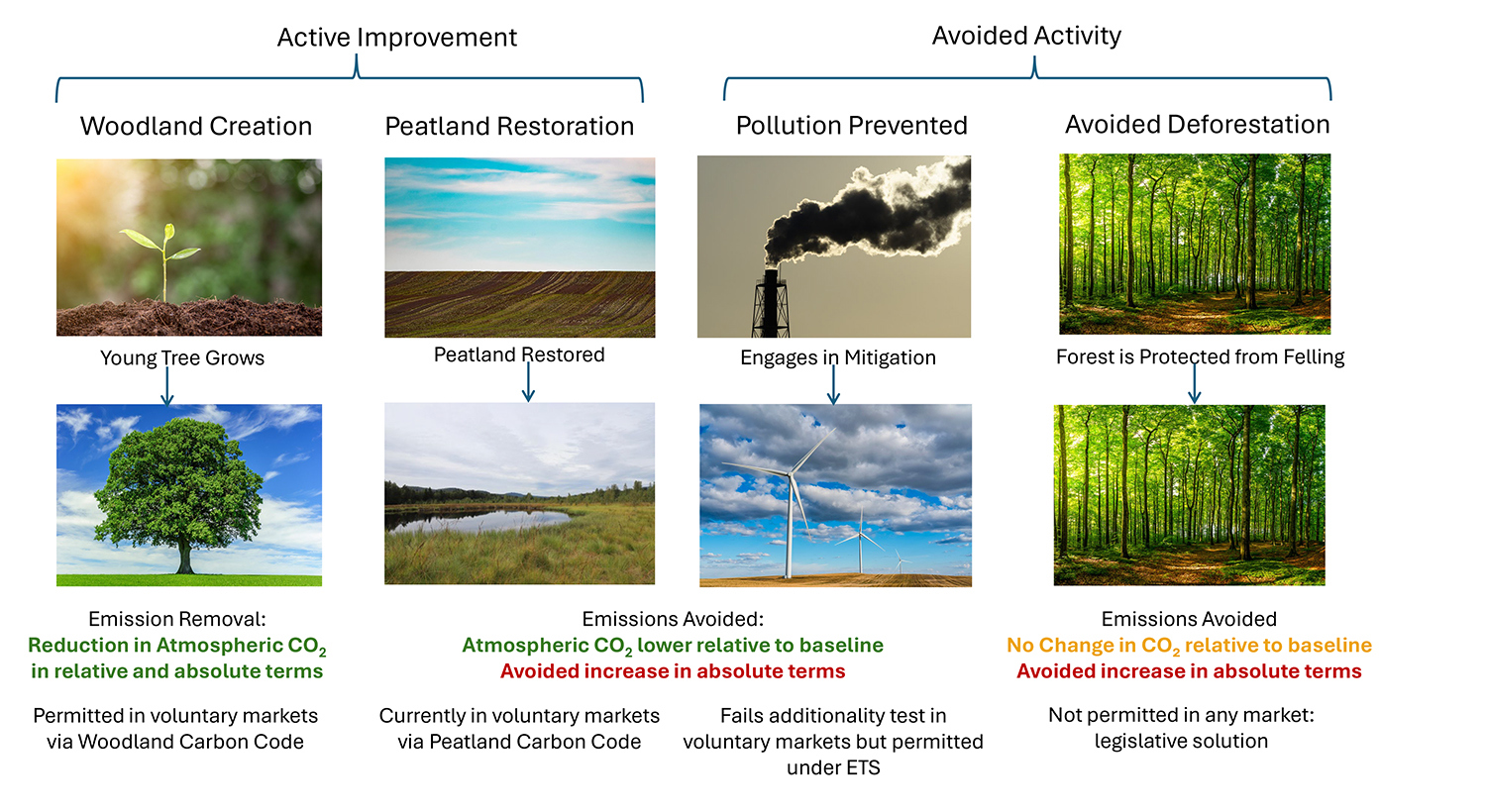

By contrast, voluntary offset markets generate credits by sequestration (Dicks et al. 2020). For example, under the Woodland Code a landowner can plant trees and sell credits from sequestered carbon to offset unavoidable emissions. The scheme is government backed but not mandatory, relying on buyers placing a premium on “green” products. This can limit the effectiveness of the scheme: while higher prices may be needed to bring more land into the scheme, businesses who are unable to pass on those costs may choose to opt out.

Figure 2. Illustrative diagram of the process of voluntary carbon markets (image created by JNCC).

To give consumers confidence that offsets reflect a genuine reduction in emissions, landowners must demonstrate “additionality.” They can only sell credits for new sequestration: not from existing woodland or woodland that would have been planted anyway. Nor can they sell credits against the sometimes substantial emissions reductions that can result from land use change (particularly when the land was previously used for livestock). More recently, government and industry has sought to address greenwashing by setting more stringent standards that incorporate the principle of additionality.

While this principle works for woodland it creates challenges for peatland restoration. Peatlands are both a source and sink of emissions depending on their condition. Restoring all three million hectares of UK peatland would reduce emissions by around 20 million tonnes of CO2 per year, not including sequestration, and is generally a highly cost effective approach to reducing carbon emissions (Moxey 2011). Just as with tree planting, landowners can receive payment through the peatland code. Like the woodland code this is a voluntary market where business pay to offset emissions. However, unlike the woodland code buyers are paying landowners for emissions reductions rather than removals.

Figure 3. Illustrative example of markets today (adapted from UK ETS Consultation Response from IUCN UK Peatland Programme (original image created by Ridge Carbon Capture Ltd).

This creates a challenge. In relative terms a tonne of avoided CO2 is equal to a tonne of sequestered CO2. But, in absolute terms reducing carbon emissions is not the same as removing carbon. Unlike paying for avoided deforestation, which clearly fails the test of additionality, peatland cannot be restored through inactivity alone. Peatland restoration sits in a grey area, more similar to allowance trading through ETS but there are questions whether this type of trading meets the standard of additionality established for voluntary markets.

Peatland also shares a problem in common with woodland: prices are too low to meet government targets. The obvious solution is to combine offsetting from voluntary markets with compliance-based ETS. Participants in ETS cannot opt-out and are thus willing to pay more for credits. ETS carbon prices are already more than double those under the voluntary market and will likely rise further (DESNZ 2023).

In 2024 DESNZ launched a consultation on just this approach for woodlands (DESNZ 2024). For now, however, the government has ruled out extending it to peatlands. Landowners may continue to receive payment through voluntary markets but this may not be sustainable in the long run. The UK cannot reach a net zero target unless sequestration matches emissions. This must eventually preclude one party from offsetting their emissions by purchasing reductions from another.

Figure 4. Illustrative diagram of Combined voluntary markets and ETS.

This leaves only two options for government to realise the readily available and cost-effective benefits of peatland restoration. Either use public money to pay landowners for avoided carbon, or charge landowners for emissions on their land. However, this is not a binary choice: there is no requirement that government cannot leverage both payments and charges and a combined approach may take better advantage of the benefits of each approach while mitigating the negatives.

An alternative approach

The ETS already awards free allowances to polluters. Those who fail to meet the target must purchase additional allowances while those who exceed the target can sell their excess allowances. The ETS supplements this process with an auction, which allows government to set maximum and minimum prices, but otherwise functions as a normal cap and trade. The EU reports that in its version that up to 57% of allowances will be auctioned from 2021 to 2030 with the remainder issued free. Though they may be forced to buy allowances if the peatland degrades further

These allowances avoid imposing an undue burden on businesses and they prevent consumers switching to less regulated imports. If peatlands were included in ETS landowners could be awarded allowances up to 100% of the emissions resulting from degraded peatland (though they may be forced to buy allowances if the peatland degrades further). If they restored the peatland they would be free to sell those allowances along with additional allowances they received for sequestration.

Government could choose to reduce the number of allowances in line with peatland restoration targets, or set intermediate targets. This would not put specific obligations on any one farmer but it would more than double payments to farmers (at current prices) who chose to restore peatland, with significantly higher payments in future years, without imposing the full burden of this cost on public funds.

Figure 5. Illustrative diagram showing the Integration of peatland into the ETS with free allowances.

Benefits

Costs and benefits of rewetting vary considerably based on how the land is being used. Conservatively, restoring all peatland would eliminate 20 million tonnes of carbon emissions annually, not including sequestration or emissions associated with farming the land. For productive peatland the largest cost will be the income foregone due to the loss of productive farmland. In some case the expansion of paludiculture – farming on rewetted peatland – could mitigate this lost income. In other cases the land may be marginal and the opportunity cost low or zero.

The Office for National Statistics estimates restoring all Peatland in the UK would cost £8–22 billion over the next 100 years with economic benefits of £109 billion from reduced carbon emissions (2019 estimates). Though harder to quantify, restoring peatland also generates nature benefits include cleaner water and reduced flood risk. The Climate Change Committee estimates achieving Net Zero requires restoring 79% of upland peat and half of lowland peat.

Bringing peatland into ETS would both provide finance to achieve this goal while incentivising landowners to deliver emissions reductions at the lowest possible cost.

Published: .